T. Rowe Price: Sandwich Generation Strain Negatively Impacts Kids and Their Money Habits

Parents who care for both their kids and an aging family member are more reluctant to discuss money with their kids and miss opportunities to talk to them about it

News

T. Rowe Price’s 2019 Parents, Kids & Money Survey, which sampled 1,005 parents of 8 to 14 year olds and their kids, found that stress among parents who are caring for both their kids and aging family members, commonly known as the sandwich generation, is negatively impacting their money habits and their kids’ money habits.

“The data are clear that balancing care for two generations simultaneously can be difficult” says Stuart Ritter, CFP®, a senior financial planner at T. Rowe Price and father of three. “Members of the sandwich generation are in a tough situation, and one of the best things they can do to support their kids is share with them the challenges that are affecting the family’s money and time.

“Parents who are dual caregivers are less likely to teach their kids about money and support them in other ways. But having money conversations can be a powerful way to bridge their understanding and impart valuable financial lessons. Talk to them about your financial life and the tradeoffs you’re making when they’re young and as they grow into adulthood. This transparency can position them to better handle financial challenges when they become adults,” says Mr. Ritter.

To help parents discuss money with their school-age kids, T. Rowe Price created MoneyConfidentKids.com, which provides free online games for kids; tips for parents that are focused on financial concepts such as goal setting, spending versus saving, inflation, asset allocation, and investment diversification; and classroom lessons for educators.

Sandwich generation is financially strained

-

More than a third of parents with 8 to 14 year old kids are caring for an aging family member: 35% of parents with 8 to 14 year old kids are dual caregivers, caring for both their kids and an aging parent or relative. 68% of them report that their aging parent or relative is living with them.

-

Caring for aging parents can be expensive: Nearly one-third (31%) of dual caregivers spend $3,000 or more a month caring for an aging parent or relative. 34% spend $1,000 - $2,999 each month, and 35% spend less than $1,000. 74% of all parents caring for an aging parent or relative say they are not receiving any kind of financial aid or support from social services to help care for their family member.

-

The expense of caring for aging family members causes financial strain: 74% of dual caregivers agree with the statement, “Caring for my parent/ relative causes financial strain.”

-

Parents who are dual caregivers are more likely to carry a credit card balance and have balances more than $5,000: 63% of parents who are caring for an aging family member regularly carry a credit card balance, compared with 37% of parents who are not caring for an aging family member. Additionally, among dual caregiver parents with credit card debt, 70% of them have $5,000 or more in credit card debt, compared with only 34% of parents with credit card debt who are not caring for aging family members.

-

Dual caregivers are significantly more likely to have pulled from retirement and college savings: Parents who are caring for an aging family member are more than three times as likely to have pulled money from their retirement savings (77% vs. 23%) and more than six times as likely to have withdrawn money from their kids’ college savings (71% vs. 11%).

Financial strain of the sandwich generation impacts kids

-

Kids of dual caregivers feel their parents don’t make enough time for them: 73% of parents caring for an aging family member say that it takes away from time with their kids—and the kids agree. Kids of dual caregivers are nearly three times as likely (59% vs. 20%) to agree with the statement, “My parents do not make enough time for me.”

-

Kids of dual caregivers say their parents worry about money: Kids of dual caregivers are more likely to say that their parents worry about money (72% vs. 45%), compared with kids whose parents aren’t caring for an aging parent.

-

Parents who are dual caregivers are more likely to be reluctant to discuss money with their kids: While half of all parents (50%) have some reluctance to discuss money with their kids, parents who are caring for an aging family member in addition to their kids are particularly reluctant. Dual caregivers are more likely to have some reluctance to discuss money with their kids (73% vs. 37%), compared with parents who are not caring for an aging family member.

-

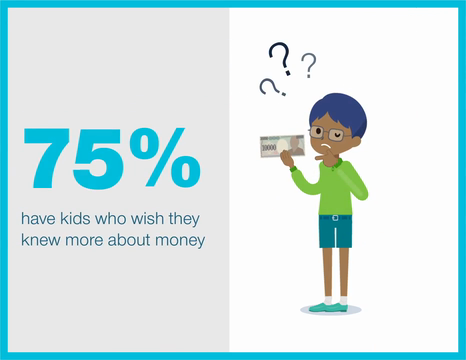

Kids of dual caregivers wish their parents taught them more about money: Kids of parents who are caring for an aging family member are more likely (75% vs. 41%) to agree with the statement, “I wish my parents taught me more about money.”

-

Parents who are dual caregivers miss more opportunities to teach their kids about money: Dual caregivers are more likely to agree with the statement (70% vs. 35%) “I miss opportunities to talk to my kids about money.”

-

Kids of dual caregivers are more likely to spend their money right away: Kids of parents who are caring for an aging family member are more likely to agree with the statement (70% vs. 49%), “I like to spend money as soon as I get it.”

-

Kids of dual caregivers are given money without guidance: Dual caregivers are more likely (62% vs. 15%) to say that they have no idea what their kids spend their allowance on and have kids who spend their allowance right away (77% vs. 41%). Dual caregivers are also more likely to give an allowance without requirement to earn it (32% vs. 8%).

MONEY CONFIDENT KIDS is a registered trademark of T. Rowe Price Group, Inc.

About the survey

The eleventh annual T. Rowe Price Parents, Kids & Money Survey, conducted by Research Now, aimed to understand the basic financial knowledge, attitudes, and behaviors of both parents of kids ages 8 to 14 and their kids ages 8 to 14. The survey was fielded from January 17, 2019, through January 23, 2019, with a sample size of 1,005 parents and 1,005 kids ages 8 to 14. The margin of error is +/- 3.1 percentage points. All statistical testing done among subgroups (e.g., those who are caring for an aging parent) is conducted at the 95% confidence level. Reporting includes only findings that are statistically significant at this level.

About T. Rowe Price

Founded in 1937, Baltimore-based T. Rowe Price Group, Inc. (NASDAQ-GS: TROW) is a global investment management organization with $1.07 trillion in assets under management as of February 28, 2019. The organization provides a broad array of mutual funds, subadvisory services, and separate account management for individual and institutional investors, retirement plans, and financial intermediaries. The company also offers a variety of sophisticated investment planning and guidance tools. T. Rowe Price's disciplined, risk-aware investment approach focuses on diversification, style consistency, and fundamental research. For more information, visit troweprice.com or our Twitter, YouTube, LinkedIn, Instagram, and Facebook sites.

Contact us

Heather McDonold

T. Rowe Price

410-345-6617

heather_mcdonold@troweprice.com

Monique Bosco

T. Rowe Price

410-345-5740

heather_mcdonold@troweprice.com